Qn1. How has your journey been since acquiring Compuscan CRB in 2019?

Since the acquisition of Compuscan CRB in 2019, Experian Uganda CRB has grown its product offering. Our clients can now access world-class credit decisioning tools and software. Advanced credit analytics and decisioning tools allow clients to make better business decisions.

Through the combined legacy Compuscan products in Uganda, and the Experian suite of solutions, we can empower consumers and companies to pursue their fundamental ambitions.

To do this, we leverage the power of data and analytics to create opportunities, improve lives and make a difference to the Ugandan consumers, businesses and economy.

We enable companies to make quick and smart decisions, thereby helping more people access the services they need. We use data responsibly by adhering to regulations, investing in technology, people, and continuous innovation.

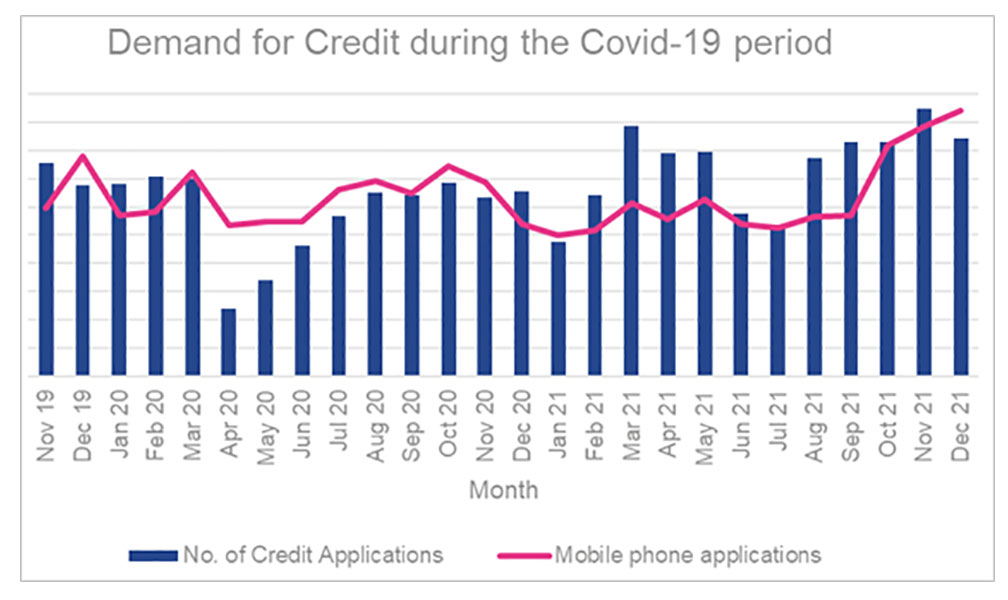

Qn2. What is/ has been the level of creditworthiness in Uganda since the break out of Covid-19?

Since the breakout of Covid-19, Uganda has seen a fluctuation in the demand and supply of credit following the government’s initiatives to control the spread of Covid-19.

In April 2020, the total number of credit applications registered on the bureau had reduced by 66% month-on-month between March 2020 and April 2020.

Of the April volumes, 68% were through mobile. Despite the abrupt reduction in the number of applications between March and April 2020, the number of applications increased over the months, with April 2020 to April 2021 seeing an increase in year-on-year volumes of 232%.

Recent figures reflect a 49.9% increase year-on-year from November 2020 to November 2021. In November 2021, we observed the highest number of applications registered on the bureau, 28% of which only were accessed through mobile phones.

With the lifting of the lockdown and the full opening of the economy, we expect the demand for credit to increase.

Qn3. Why is the use of the financial cards/ financial card system penetration still low? Where’s the missing link?

The current regulations limit the use of credit reference bureau services (and the Financial Card system) to regulated financial institutions by the Bank of Uganda.

The current penetration of the credit reference bureau services is approximately 6.5% of the credit-active population, with the majority of the credit issued within the non-regulated financial sector, which is not reported and therefore not on the credit reference bureau.

Although the Financial Institutions Act was revised in 2016 to enable the use of the credit reference bureau services by accredited credit providers, the implementing regulations are still being formulated and reviewed by the Bank of Uganda, the regulatory body of the financial sector.

With the expansion of the credit reference bureau use to include the non-regulated lenders, we expect the penetration of the financial card system and the credit reference bureau to grow.

Qn4. As Experian, what do you intend to achieve in Uganda in the next five years?

Over the next five years, we intend to empower Ugandan businesses to make better, quicker, and smarter business decisions.

Through our user-permissioned data, robust analysis and insights, combined with our world-class delivery platforms and continuous investment in technology and innovation, our clients can reduce the risks associated with lending, improve their customer experience and establish efficient business processes.

One of Experian Uganda’s key innovation strategies is to develop insights for commercial needs while making a positive difference to those in financial need.

We are committed to driving financial inclusion, improving credit access, and accelerating innovation in Africa for consumers. Experian brings improved infrastructure and data platforms for increasing financial inclusion and development in Uganda.